Sales Tax Consultant Having Success Recovering Georgia Sales Tax Refunds for Hospitals & Healthcare Industry

Georgia sales tax exemption refunds for healthcare providers, including hospital, clinics, and medical practice groups include several categories of purchases. One Georgia sales tax exemption for healthcare providers that a sales tax consultant from Agile Consulting Group has been recovering a significant amount of refunds for relates to prosthetic devices. Georgia Code Ann. § 48-8-3(54) states that prosthetic devices that are sold or used pursuant to a prescription are exempt from Georgia sales and use tax. Our sales tax consultant has learned that the prosthetic device may be purchased exempt from Georgia sales and use tax by a hospital, clinic, or medical practice group if it is sold or used pursuant to a prescription under federal or state law and title and possession is permanently transferred to a natural person to whom a prescription for the device is issued, per Georgia Comp. Rules & Regulations § 560-12-2-.30(5)(a).

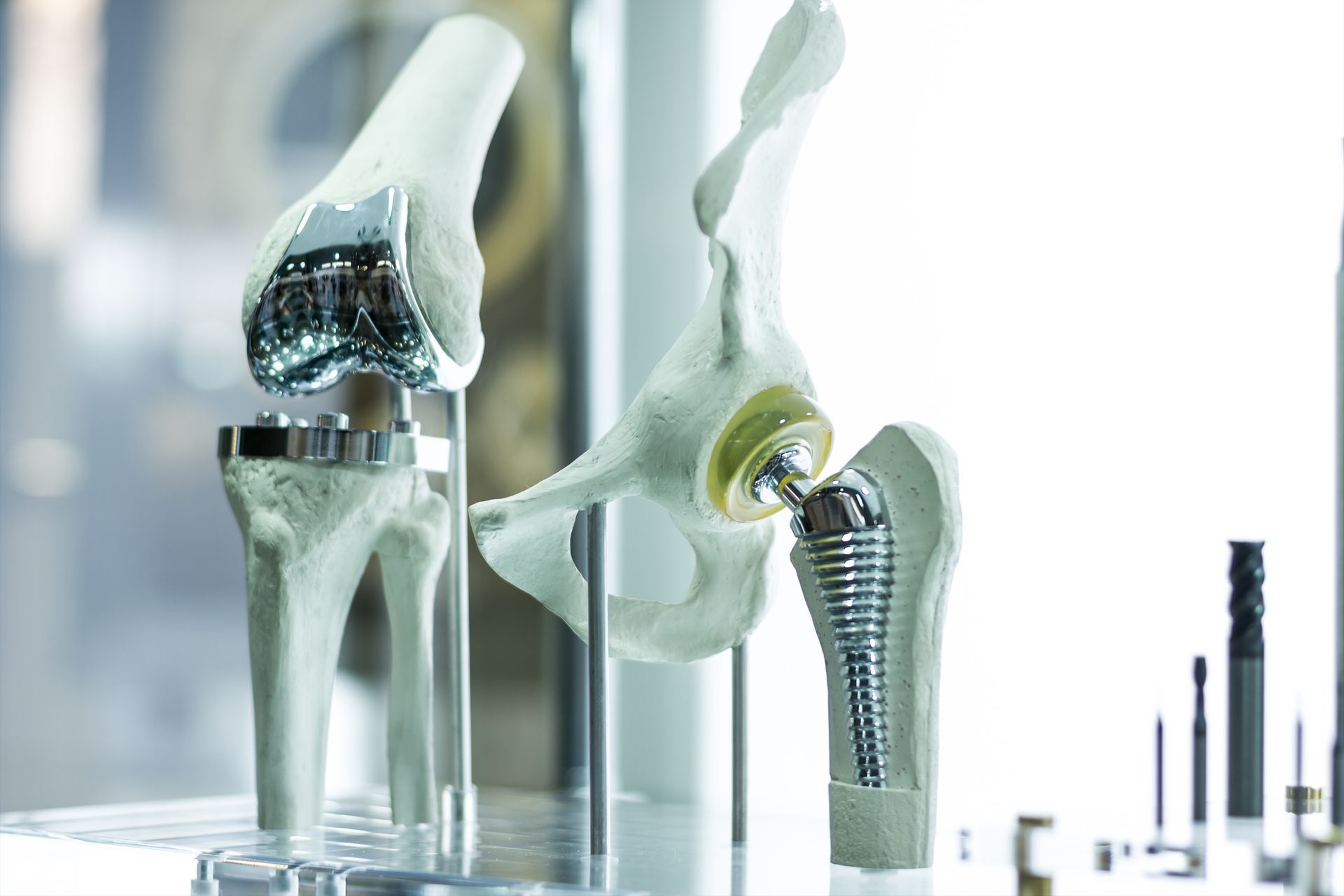

A prosthetic device is defined in Georgia Comp. Rules & Regulations § 560-12-2-.30(2)(h)(1) as, “a replacement, corrective, or supportive device including repair and replacement parts for the same worn on or in the body to either artificially replace a missing portion of the body; or prevent or correct physical deformity or malfunction; or support a weak or deformed portion of the body.” An item does not need to meet all three of these criteria to qualify as a prosthetic device. As long as the item meets at least one of these criteria, it will qualify for a sales and use tax exemption in Georgia. Some examples of prosthetic devices include:

-

- Artificial implants such as vascular stents, heart valves, intraocular lenses, collagen tissue, bone nails, bone screws, bone fixation devices, or bone cement

- Cardiac pacemakers and implanted cardioverter defibrillators

- Surgical mesh

- Gastric bands and intragastric balloons

- Colostomy, ileostomy, and urostomy appliances, including bags and necessary equipment required for attachment

- Urinary collection systems including Foley catheters, when replacing bladder function in cases of urinary incontinence

- Enteral or parenteral feeding systems and their individual components

- Braces, cervical collars, abdominal belts, anti-embolism stockings, compression garments and similar devices worn on the body to correct or alleviate a physical incapacity or injury

Additionally, our sales tax consultant has been successful recovering Georgia sales and use tax refunds for most types of wound care dressings as these items have been determined to qualify as prosthetic devices since they alleviate physical incapacity or injury. Some examples of wound care dressings that qualify are bandages, gauze sponges, gauze bandages, splint trapping material, barrier film spray, gel sheets, absorbent pads, packing strips, and closure strips.

In order to claim these Georgia sales tax exemption refunds on future qualifying purchases of prosthetic devices, Georgia healthcare providers must supply their vendors with a valid Georgia sales tax exemption certificate. The proper form that should be completed is the Georgia Streamlined Sales and Use Tax Certificate of Exemption (ST-5 SST). This certificate can be found at the Georgia Department of Revenue website. For healthcare providers who have already paid the Georgia sales tax to their vendors or remitted use tax to the Georgia Department of Revenue on qualifying exempt prosthetic devices, they can complete the ST-12 Claim for Refund form. For sales tax refunds, the applicant must also get an ST-12A Waiver of Vendors Rights for Refund form signed and notarized by each vendor that charged Georgia sales tax. An application for a refund must be submitted within three years from the date of payment. This refund claim form can also be found on the Georgia Department of Revenue website.

As with all sales and use tax research, the specifics of each case need to be considered when determining taxability. Additional advice from Agile Consulting Group’s sales tax consultant can be found on our page summarizing Georgia sales and use tax exemptions. If you have questions, comments or would like to discuss the specific circumstances you are encountering regarding this issue or any other sales and use tax issue, please contact a sales tax consultant at (888) 350-4TAX (4829) or via email at info@salesandusetax.com.